Last Updated: April 19, 2021

Introduction:

The apparel sector has traditionally been a gateway to export diversification and industrial development for low-income countries (LICs). While there’s no consensus among scientists regarding the origins of apparel, one thing is certain: Apparel has come a long way over the centuries, from materials used and production methods to added functionality and styles. As it continues to evolve, so does the global apparel retail industry, which in 2011 was valued at $1.175 trillion. According to Statista.com, the global apparel market is projected to grow in value from 1.5 trillion U.S. dollars in 2020 to about 2.25 trillion dollars by 2025, showing that the demand for clothing and shoes is on the rise across the world.

With the present transient status of many countries’ economies, the international textile industry faces considerable challenges. There are many uncertainties surrounding the global textile market, exacerbated by the foreboding that in 2005, quotas will be eliminated, resulting in “free” trade flows. There is no doubt that manufacturers who have created niche markets will be better positioned to compete in the global marketplace and achieve higher margins for products while yielding greater profitability.

Since 2005, the global apparel and textiles market has both expanded in value and consolidated in suppliers. The top ten developing country suppliers now make up 58% of global apparel exports, with Asian suppliers accounting for 52% in 2011. The top exporters of apparel have also been amongst the main exporters of textiles. In 2011, global apparel exports were worth over USD 412 billion, while global textile exports reached USD 294 billion.

Developing Country Suppliers and the Global Apparel Market, 2005-2011

Between 2005 and 2011, the value of global apparel exports rose by 48%. Globally, apparel exports were worth USD 412 billion dollars in 2011. The top ten developing country suppliers now account for 58% of global apparel exports, with China taking 37% of that share in 2011 (see Table 1).

Table 1: Developing country suppliers and the global apparel market (2005-2011, USD million, current)

Asian exporters in particular have consolidated their role as the principal exporters of apparel products. Export growth of apparels outside Asia has also been positive. In fact, some of the fastest growth in export sales has been recorded outside the Asian region (see Table 2), albeit from a very low base in most cases. With the exception of Chile, Egypt, Ethiopia and Panama, the rest of the fastest growing apparel exporters were marginal in global terms, exporting less than USD 10 million in 2011 – and in three cases less than USD 1 million.

Table 2: Fastest growing apparel exporters (2005-2011, USD million, current)

Other developing country suppliers have seen their export sales slide and some might have exited apparel production altogether between 2005 and 2011 (see Table 3). The suppliers that experienced the biggest drop in export sales were the Dominican Republic (-66%), Costa Rica (-64%), Swaziland (-51%), the Philippines (-39%), Mexico (-37%) and Chinese Taipei (-36%). Apparel manufacture has all but ceased in certain marginal exporters, like Belize, the Maldives and Zambia.

Table 3: Suppliers with falling apparel export sales (2005-2011, USD million, current)

Declining apparel exports from the Dominican Republic, for example, contrast sharply with Haiti, whose apparel exports grew by 72% to reach USD 677.4 million in 2011. Labour price differentials may explain some of the divergence in performance, together with differing rules of origin in trade agreements.

Together, the European Union, the United States and Japan account for 72% of global imports of apparel in 2011. This share has fallen by 14% since 2005 as other import markets have grown in value. Imports to other OECD destinations e.g. Canada, Korea and Australia have grown in the range of 60-109% (see Table 4).

Table 4: Apparel import markets (2005-2011, USD million, current)

Import growth of between 65% and 132% has also been recorded by Brazil, Chile, China, India, Russian Federation, and Thailand between 2009 and 2011. Together, these six markets accounted for USD 17.1 billion in clothing imports in 2011 – up from USD 3.9 billion in 2005 – but still only 4% of total apparel sales, a statistic that underscores the scope for further growth in these markets as incomes rise.

Tables 5 and 6 highlight the penetration of developing country suppliers in apparel exports to the United States and the European Union. These tables identify the top 15 apparel exporting countries to the US and EU.2 In 1970, Hong Kong, the Republic of Korea, the Philippines, Mexico, Israel, and Singapore, were among the top 15 countries for garment exports to the United States. Japan, which joined the Organization for Economic Co-operation and Development (OECD) in 1964, headed the list of apparel producers in 1970. In 1980 China, Dominican Republic and Sri Lanka joined the top 15 exporting countries from the developing world, while India, Indonesia, Malaysia, Thailand and Bangladesh were added in 1990. Since 2000, China headed the list of apparel exporters to the US and European Union.

Table 5: Top 15 Apparel Exporters to the United States

The emergence of developing country suppliers is also apparent as regards apparel exports to the EU (Table 6). Turkey’s penetration of its neighboring EU market is clear from the table. While Turkey has been the second largest exporter to the EU since 2000, it does not appear in the list of the top 15 suppliers to the US. The same is also true of Tunisia and the FYR Macedonia. Likewise, while Honduras and Nicaragua appear in the list of the top 15 suppliers to the US, they do not appear among the same list for the EU. Geographical proximity, combined with preferential market access, may be an explanatory factor.

Table 6: Top 15 Apparel Exporters to the European Union

Changing Market Access Conditions:

From 1974, the Multi-Fibre Arrangement (MFA) governed the international textiles and apparel trade. A large portion of textiles and clothing exports from developing countries were subject to bilaterally negotiated quotas. In 1995, the MFA was replaced by the WTO Agreement on Textiles and Clothing (ATC), which set out a 10-year transitional process for removal of these quotas. With the expiry of the ATC on 1 January 2005, global apparel trade was no longer subject to quantitative restrictions. Other “market distortions” remain, however, notably in the form of tariff escalation, tariff peaks, export competition measures and non-tariff barriers.

Various duty-free quota-free (DFQF) access for LDC exporters have been established by developed and some emerging economies (see Box 1). Developed Members’ GSP schemes play a major role in defining global market access conditions in textiles and apparel markets. Other non-reciprocal preferential access schemes, such as the US’s African Growth and Opportunity Act (AGOA) grant preferences to eligible countries in Sub-Saharan Africa. An extensive body of literature has also been authored on how rules of origin applying to preferential market access schemes affect utilization rates. Both preferential rules of origin and DFQF access remain areas of negotiation in the Doha Development Agenda.

Other trade policies also exert an influence on value chain dynamics. For example, both Chile and Panama have signed Free Trade and Trade Promotion Agreements with the US and Free Trade Agreements with the EU. Agreements signed by Egypt with the EU (EU-Egypt Association Agreement) and the US (Agreement on Trade and Investment Relations) may also be a contributory factor in that country’s growing apparel exports. Both the US’ African Growth and Opportunity Act (AGOA) and the EU’s African, Caribbean and Pacific (ACP) scheme may also help explain growth among African markets in Table 7.3 Turkish investment in Azerbaijan together with its Partnership and Cooperation Agreement with the EU may also have contributed to some of the rise in Azeri apparel exports.

Table 7: Fastest growing and fastest falling African exporters of apparel (2005-2011, USD million, current)

Preferential schemes have undoubtedly helped some low-income countries, but their impact has been mixed as far as the export performance of other countries is concerned. This is the case among Africa exporters who posted differing performance in this value chain during this period.

Sharp declines were registered in South Africa, Swaziland, Malawi, Mozambique, Namibia, Zambia, and Côte d’Ivoire. Despite the possibility to develop a fully integrated African apparel sector, benefiting from proximity to the region’s abundant supply of cotton and textiles, Africa remains a net exporter of cotton and a net importer of textiles and clothing.

For all but a few African countries, low-income levels do not automatically translate into a comparative advantage in low-wage basic apparel manufacture. Other important constraints are the availability and cost of key backbone services, transportation, labour skills and a stable business climate. A recent survey of labor costs and productivity in selected African countries relative to comparators using data for 25 countries from the World Bank’s Enterprise Surveys concludes that industrial labor costs are higher relative to GDP per capita than in comparator countries. Part of the explanation lies in a steep labor cost curve; as firms grow larger and more productive their labor costs increase faster in Africa than elsewhere. (Gelb, Meyer and Ramachandran, 2013). Specifically, in the garment industry, a firm-level study demonstrates that production costs in Kenya are measurably higher than those in Bangladesh, not because of lower productivity, but due to higher labour costs in Kenyan firms (Fukunishi, 2009).

Developing Country Suppliers and the Global Textiles Market 2005-2011

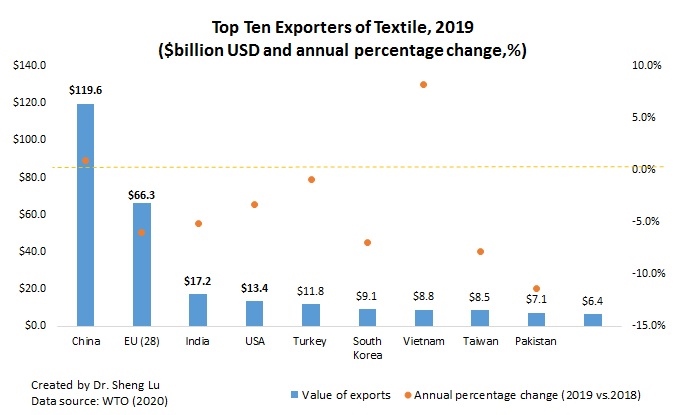

In general, the top exporters of apparel have also been amongst the main exporters of textiles. The fastest growing exporters of textiles in the period 2005-2011 were: Egypt (+446%), Viet Nam (+420%), China (+130%), Bangladesh (+125%), India (+80%) and Turkey (+52%). With the exception of Egypt, the other nine countries amongst the top ten exporters of textiles came from Asia (see Table 8).

Table 8: Fastest growing exporters of textiles (2005-2011, USD million, current)

There are exceptions to the pattern of registering gains both in textiles and apparel exports. While the Dominican Republic registered a dramatic decrease in its apparel exports (-66%), it posted, although in very modest volume terms, an even higher upswing in its textiles exports (+1,000%). Likewise, Chinese Taipei’s apparel exports shrank abruptly (-36%) but, in parallel, its textiles exports increased (+14%). While the Republic of Korea saw its apparel exports decline (-29%), its exports of textiles products increased (+19%). Similarly, in Romania, apparel exports declined significantly (-27%) while textiles exports increased (+81%). In Côte d’Ivoire, apparel exports contracted markedly (-72%) while its textiles exports posted important gains (+63%).

The textiles and apparel sectors are often treated as one industry with similar economic characteristics. However, they are two sectors with very different technological dimensions, particularly in factor intensity. They are connected through strong backward and forward linkages in a vertical production and distribution network; however, the textiles sector is in general much more capital intensive than the apparel sector.

The textiles sector (yarn and fabrics) comprises a wide range of products, which can roughly be classified into natural fiber based products (such as cotton, wool, or silk yarn and fabrics) and synthetic fibre based products (such as nylon or polyester yarn and fabrics), each with significantly different production technology and industrial organization attributes. The former is closely linked to the agricultural sector; however, the latter has strong backward linkages with the chemical oriented industries and is more capital intensive. As such, developing countries with abundant labour but low levels of capital accumulation do normally not exhibit strong comparative advantages in the production of synthetic fibre and related products.

As the production of textiles also requires higher levels of technological contents, workers’ skill and knowledge base also become critical. The natural fibre sub-sector, on the other hand, is typically less capital and technology intensive. Natural resource endowments are clearly important to the development of this sub-sector. However, resource endowments do not automatically translate into export competitiveness due to factors related to the business environment. Some LDCs are also concerned about the impact of export competition on the competitiveness of their cotton growing sector. The cotton sector connects with the traditional handicraft sector, which utilizes very labour intensive technologies (although some highly skill intensive), supporting livelihoods of many in both developed and developing countries.

When textiles are used as input materials for the production of apparel, they must meet specific quality standards in terms of physical and chemical properties. These would include, for instance, quantifiable standards such as strength and dimensional stability of the fabric, abrasion and pilling resistance, and colorfastness (against light, crocking, and washing). These qualities are normally tested in laboratories against the specific standards set by global buyers in relation to the final markets they serve. In comparison to the standards set for apparel products, these requirements are more elaborate, detailed, and difficult to comply with, and deter entry of less experienced firms in developing countries into international production and distribution networks.

The apparel sector, on the other hand, is in general more labor intensive, and variation in factor intensity according to products is much smaller than that of the textiles sector. As this sector is more downstream and closer to the consumers, the designing, branding and marketing functions become crucial. These functions are undertaken by firms in developed countries, and fetch a substantial proportion of the total value-added in the chain. Developing countries typically participate in these chains by catering for the labour intensive assembly functions.

As such, while this report addresses both the textiles and apparel sectors, for the sake of analytical clarity, it mainly focuses on the apparel sector. However, as the production systems for some type of apparel products, such as knitted apparel, are more vertically integrated and division between these two sectors is less clear than others, we will address textiles sector specific issues whenever necessary.

The World Scene: Intensifying Competition in the run up to the abolition of MFA

World export of textiles and clothing1 amounted to about US $ 356 billion in 2000, or, 6 percent of world exports, with the relatively labor-intensive clothing sector valued higher than textiles at US $ 199 billion. Since 1962, when Japan became the first dynamic exporter, importing industrial countries have sought to limit import penetration by exporters under various quantitative controls such as “Long-Term Agreements” (1963-74), “Multi-Fiber Arrangement” (1974-94), and, the current ly in force, “Agreement on Textile and Clothing” (1995-2004). While the pace of growth in textile exports has always lagged behind that of manufactures, clothing sector outpaced it through the 1970s and 1980s, but witnessed a slowdown since the 1990s (Figure 1). Particularly, under the current phase of ATC, growth has been negative in the run up to the total lifting of all quantitative restriction on January 1, 2005.

The weakness in growth witnessed in last decade, measured in current US dollar values, is attributable in part to intense competition among exporters2 (the share of top 10 countries in EU and US markets, for example in clothing, have declined from 65 to 53 percent and 84 to 59 percent, respectively, over 1980 to 2000), the slump in raw material prices of cotton (near 50 % drop in cotton prices between 1995 and 2001), and the strong productivity gains in the textile sector (27 of the 43 countries registered a decline of 8 to 59 % in labor costs relative to US between 1990 and 2000).

The two main markets for textile and clothing imports are Unites States and EU, roughly accounting for US 82 billion and US $ 71 billion, respective ly, in 2000. The other industrial countries of Canada and Japan and Australia together accounting for US 33 billion. In the second half of the 1990s, the US market has overtaken the EU market (extra-EU) by growing nearly thrice as fast.

References:

- Apparel Market: Landscape Of Change by Textile World

- https://www.statista.com

- Dynamics in apparel global value chains and implications for low-income countries-by Cornelia Staritz

- Textile and Clothing Exports in MENA Past Performance, Prospects and Policy Issues In Post MFA Context-by Masakazu Someya, Hazem Shunnar and T.G. Srinvasan

- Reportlinker.com

- Aid for Trade and Value Chains in Textiles and Apparel

- Opportunities in the international textile and apparel marketplace for niche markets-by Erin Dodd Parrish, Nancy L. Cassill and William Oxenham

- World Trade Organization database.

You may also like:

- Textile Industry in Pakistan – An Overview

- Ready-Made Garments (RMG): The Leading Earning Sector in Bangladesh

- Prospects of Garments Industry in Bangladesh

- An Overview of Indian Textile Industry

- Garments Made in India: Why Quality is Factor?

- Overview of the Vietnam Textile and Garment Industry

- Sri Lankan Apparel Export Position in Global Market

Founder & Editor of Textile Learner. He is a Textile Consultant, Blogger & Entrepreneur. Mr. Kiron is working as a textile consultant in several local and international companies. He is also a contributor to Wikipedia.